Homeowners associations (HOAs) rely on contractors for important construction and maintenance work. However, these crucial jobs come with risks to the HOA, its residents, and the contractor. Accidents and mistakes happen, even with reputable contractors, and that’s why most contractors carry insurance to protect themselves and their clients. If your HOA is hiring a contractor, it’s always wise to check their insurance coverage. This guide will help you understand the importance of HOA contractor insurance and proof of insurance requirements for HOA vendors.

What Is Contractor Insurance?

Contractor insurance can refer to any or all types of insurance covering contractors. When working for HOAs, this insurance includes general vendor liability coverage that pays out if the contractor damages property or injures anyone while working in the community. The contractor pays for this insurance through monthly or annual premiums, and the insurer pays out under specified conditions to protect the contractor and your HOA from financial and legal liabilities.

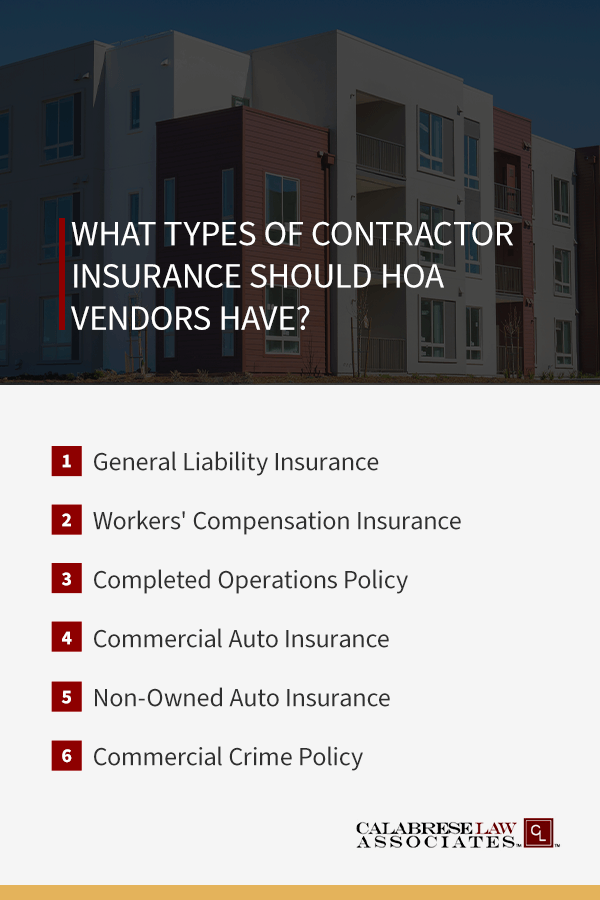

What Types of Contractor Insurance Should HOA Vendors Have?

Contractors may carry any or all of the following six types of insurance that HOA board members should know about.

1. General Liability Insurance

This insurance is the most common and important type of policy an HOA wants its contractors to have. It protects the contractor and the HOA from liability should the contractor cause bodily or property damage while on the premises. For example, the contractor’s insurer would compensate a homeowner if the contractor cut down a tree that fell on their car or injured them.

2. Workers’ Compensation Insurance

This insurance covers medical expenses and lost wages if any of the contractor’s employees become injured for job-related reasons while working in the HOA community. This policy type protects the HOA and the contractor from needing to compensate injured workers.

3. Completed Operations Policy

Sometimes, a contractor’s work causes damage after the project is complete. For example, a deck installed near the HOA clubhouse could collapse years after the project’s end. A contractor’s completed operations insurance policy can cover the resulting costs, protecting the contractor and the HOA from heavy financial burdens. This type of coverage is most important for structural work, plumbing, or electrical installations. Any contractor doing work that may cause gradual or delayed damage should carry this insurance.

4. Commercial Auto Insurance

Contractors and their employees sometimes drive company cars and construction vehicles while doing work for HOAs. This coverage compensates third parties if any of the contractor’s company vehicles causes them property damage or injury.

5. Non-Owned Auto Insurance

If a contractor’s employees cause accidental injuries or property damage in the HOA community while driving their personal vehicles for work purposes, this insurance covers costs outside the limits of the driver’s personal auto policy. For example, a contractor’s employee driving their own car could crash into an HOA resident’s vehicle on their way out to fetch construction supplies. In this case, the contractor’s non-owned auto insurance can pay out to pay for the resident’s repairs. HOAs may ask contractors whether they use company vehicles, personal vehicles, or both during the vetting process to evaluate what type of auto insurance is necessary.

6. Commercial Crime Policy

This insurance is less common, but some contractors carry it. Even reputable contractors sometimes have employees who end up committing crimes. When a contractor has a commercial crime policy, their insurer compensates them if an employee steals their property or money. However, if a contractor’s employee steals from the HOA, the HOA cannot claim from the contractor’s commercial crime policy because these policies usually lack third-party benefits. Instead, the HOA should take out their own crime insurance to stay protected.

Why Is Contractor Insurance Important?

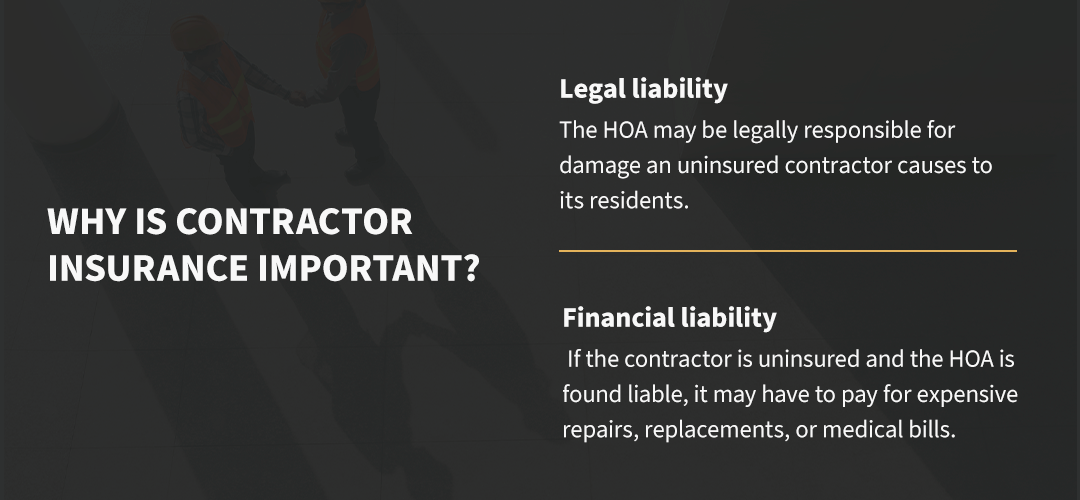

Contractor insurance is important for the contractor and the HOA. In many situations, liability for damage caused by an uninsured contractor can fall on the HOA that hired them. Liability in these situations could include:

- Legal liability: The HOA may be legally responsible for damage an uninsured contractor causes to its residents. In some cases, the HOA may face expensive and time-consuming lawsuits.

- Financial liability: If the contractor is uninsured and the HOA is found liable, it may have to pay for expensive repairs, replacements, or medical bills.

Are HOAs Required to Obtain Proof of Insurance From Contractors?

Regulations regarding HOA contractor insurance requirements vary between locations. In Massachusetts, no laws require HOAs to obtain proof of insurance from contractors. Additionally, state law does not require contractors to carry liability insurance to obtain a Construction Supervisor License. HOAs can request proof of insurance before working with contractors, and they may include this as a requirement in their bylaws. Contractors who have employees are subject to the general requirement that all employers in Massachusetts must have workers’ compensation insurance for their employees.

Whether required or not, requesting proof of insurance from contractors is always wise to protect the HOA from liability for the contractor’s actions. At a minimum, HOAs should choose contractors with general liability and workers’ compensation insurance and potentially additional forms of coverage depending on the project’s risks.

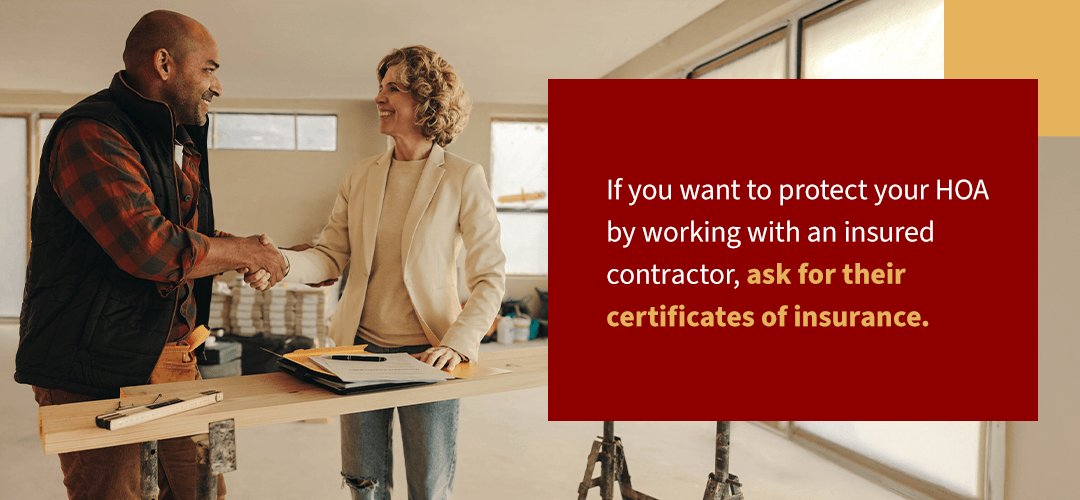

What Proof of Insurance Should HOAs Ask For?

If you want to protect your HOA by working with an insured contractor, ask for their certificates of insurance. These documents should indicate the contractor’s:

- Certificate holder identification

- Insurance company

- Policy number

- Policy period

- Insured name

- Additional insured

- Liability limits, including $1 million in liability coverage per location

Ask contractors to have their insurer add your HOA as an additional named insured on their policies. This addition gives your HOA greater rights and ensures they will cover it for any damage the contractor causes. Ask to see the contractor’s certificate of insurance listing your HOA as an additional insured after they have completed this update.

It’s also advisable to require contractors to notify the HOA within a fixed period if they have any lapse or termination of coverage, so your HOA can deny them access if they become uninsured. Even if there are no changes, your HOA may require regular contractors to provide updated proof of insurance each year. If you have any doubts, you can use the information in their insurance documents to contact their insurer and check that coverage is in force.

What Are Contractor Insurance Exclusions?

Most insurance policies have exclusions — circumstances under which they won’t pay out. Common exclusions for contractor liability insurance include:

- Intentional damage or injury

- Contractual liability

- Some instances of injury or damage related to pollution

- Damage to the contractor’s work or product

- Vehicle accidents, which auto insurance should cover

When reviewing your contractor’s insurance policies, ask if there are any unusual exclusions. If exclusions increase risks relevant to your project, check that your HOA’s insurance covers these eventualities. If the contractor’s exclusions create significant coverage gaps, your HOA should consider requiring them to close those gaps before working together.

Contractor Risk Management Strategies for HOAs

To protect your HOA from unnecessary costs and disputes, aim to develop a solid risk management plan. This plan should outline a process for identifying and mitigating risks that your HOA can follow for every project. Steps to cover in an HOA contracting risk management plan include:

- Risk assessment: Identify potential risks based on the proposed project’s scope. These could include vehicle accidents, employee injuries, bystander injuries, and property damage.

- Insurance requirements: Based on the risks, determine the insurance coverage a potential contractor should have before working in your HOA community. It’s reasonable to require all contractors to have general liability and workers’ compensation insurance. Often, your HOA may want a contractor carrying commercial auto insurance, non-owned auto insurance, or both, depending on the vehicles they intend to use. A completed operations policy is important for any projects that could lead to longer-term issues.

- Contractor vetting: Establish a vetting process to verify each potential contractor’s licensing, insurance, and track record. Contractors who pass vetting and complete quality work could go on your HOA’s preferred vendors list for future projects, provided they supply updated proof of insurance each year and meet any other requirements your HOA sets. Notify homeowners of new contractors working in the community and the vetting standards they’ve met for transparency and peace of mind.

- Contractual agreement: After selecting a contractor, draft and sign a contract with clear terms covering obligations and liabilities. Include requirements like informing the HOA of any changes to their insurance coverage within 24 hours. The contract should clarify that the contractor is independent and not an employee of the HOA to avoid liability for any mistakes. A contract law attorney with experience in HOA contracting situations can help you ensure this agreement is comprehensive and binding.

- Monitoring and review: Outline safeguards like worksite inspections and scheduled insurance verifications to ensure contractors remain compliant.

- Crisis management: Plan how to respond if an incident occurs, such as assessing the damage, communicating with affected parties, preventing further damage, documenting evidence, and consulting an attorney to confirm who is liable.

- Engagement and improvement: Allow trustees, board members, and homeowners in the community to comment on the risk management plan. Schedule regular reviews to address any unforeseen risks that emerge.

How to Manage HOA Contracting Liability Disputes

If a damaging incident happens during an HOA contracting job, liability disputes can follow. Sometimes, the situation is straightforward — a contractor causes accidental damage, their insurance pays out, and all is well. Other situations are more challenging. Disputes could happen if:

- The contractor and HOA disagree over who’s at fault.

- The contractor’s insurer refuses to pay based on a technicality.

- The incident falls into an unforeseen insurance gap.

- The contractor’s relevant insurance policy has expired.

If your HOA experiences a liability dispute for any reason, contact an attorney with expertise in the relevant areas, including HOA law, contract law, and litigation. A skilled attorney can help establish who is liable and represent your HOA in negotiations or litigation if necessary. You can often avoid litigation through communication. However, even in these cases, it’s best to have legal counsel to ensure a fair outcome. After resolving a liability dispute, consider whether updating the HOA’s risk management plan, bylaws, or contractual terms can help avoid similar situations in the future.

Why Trust Calabrese Law Associates?

Calabrese Law Associates is an industry-leading law firm serving the Greater Boston Area. Our award-winning legal team’s practice areas include HOA law, contractor litigation, construction law, condominium law, and contract law. We understand the legal challenges and nuances of liability when disputes arise between HOAs, contractors, and homeowners. The expert attorneys at Calabrese Law Associates stay updated with Massachusetts HOA and construction law to provide trusted counsel and representation to all parties involved in HOA contracting relationships.

At Calabrese Law Associates, we are attentive to our clients’ needs and have lasting relationships with individuals and associations throughout the Greater Boston Area. This experience allows us to understand legal issues affecting HOA contracting on a human level as well as through legal knowledge and litigation experience. Multiple Clients’ Choice awards and testimonials reflect our legal expertise and high service standards in real estate, construction, and contract law.

Contract Calabrese Law Associates for Legal Help With HOA Contracting

If your HOA is experiencing a dispute with a contractor, their insurer, or homeowners in your community over liability for damage, you need legal advice. Calabrese Law Associates is the leading law firm practicing HOA law and contractor litigation in the Greater Boston Area. Whether you need expert counsel to draw up a contract or representation in a dispute, our award-winning legal team is here to support you.

At Calabrese Law Associates, we provide industry-leading legal services at competitive rates. Our skilled attorneys have a track record of achieving the best possible result for each client’s situation, and we provide highly attentive, accessible service. If you need help holding another party accountable, avoiding disputes through a solid HOA contracting agreement, or protecting yourself from being held liable when you shouldn’t be, our expertise is on your side.

Schedule your free consultation with an HOA contracting attorney today.