There are many ways to finance commercial real estate and construction projects in Massachusetts. Loans and mortgages are common examples. However, the laws governing these loans are complex, so we have prepared this guide to help broaden your understanding. You will learn the meaning of commercial real estate lending, some applicable regulations, and how to secure a loan.

The construction loan regulation lawyers at Calabrese Law Associates can help protect your rights and interests.

Contact Our Construction Attorneys

What Is Commercial Real Estate Lending?

Commercial real estate (CRE) lending means acquiring loans to finance the purchase, development, or refinance of commercial properties. This type of lending differs from residential real estate lending, as it focuses on properties intended for business use instead of personal residences. The primary focus is on properties that can generate income, such as:

- Hotels

- Office buildings

- Retail centers

- Manufacturing facilities or warehouses

- Multifamily housing, like condos and apartments

- Mixed-use developments

Commercial loans typically involve larger amounts than residential loans, ranging from hundreds of thousands to millions of dollars, depending on the property and project.

Commercial Real Estate Loan Regulations in Massachusetts

There are state and federal real estate and construction loan regulations to consider. These include:

1. Division of Banks Regulations

The Division of Banks oversees financial institutions in Massachusetts, including banks and credit unions that offer commercial loans. The agency enforces several regulations, ensuring a competitive, sound, and accessible financial services environment in the state. Covered areas include licensing or mortgage lenders and brokers, as well as consumer protection.

2. Real Estate Lending Standards

The Federal Deposit Insurance Corporation (FDIC) is an independent federal agency that insures deposits in banks and oversees financial institutions for consumer protection and safety. Institutions supervised by the FDIC that extend real estate credits must comply with these real estate lending standards.

3. Equal Credit Opportunity Act (ECOA)

The ECOA prohibits discrimination against loan applicants based on race, national origin, color, religion, gender, marital status, age, or public assistance status. It also requires creditors to provide applicants with reasons underlying their decisions to deny credit when requested.

4. Fair Housing Act (FHA)

The FHA covers persons or entities engaged in residential real-estate-related transactions, including loans to construct, purchase, improve, maintain, or repair a dwelling. The purpose is to prohibit discrimination on the basis of race, national origin, color, sex, religion, familial status, and disability. The FHA can apply to commercial loans secured by residential real estate.

5. Fair Credit Reporting Act (FCRA)

The FCRA promotes the accuracy, fairness, and privacy of information in the files of consumer reporting agencies. It may apply if the commercial mortgage loan involves a co-applicant, individual guarantor, or additional signatory, primarily when an individual’s creditworthiness is relied upon in making the loan. FCRA’s applicability depends on several factors, including whether the individual is personally liable for the loan and the type of report used in evaluating their creditworthiness.

Types of Real Estate and Construction Loans

There are different types of CRE loans, including the following:

- Conventional CRE loans: These are the traditional loans offered by banks, credit unions, and other lenders. The loan duration could range from five to 30 years.

- Hard money loans: These are loans secured by real estate provided by private investors instead of traditional financial institutions. They typically have higher interest rates and shorter terms.

- Commercial bridge loans: These short-term loans cover costs between the end of a construction loan and the beginning of a standard mortgage.

- Small Business Administration (SBA) loans: These loans include SBA 7(a) and 504. 7(a) loans are long-term financing for various purposes. 504 are long-term, fixed-rate financing for fixed assets that promote job creation and business growth.

CRE loans can be ideal for financing different types of investment properties.

Commercial Construction Loan Requirements

The loan requirements differ among lenders but generally include the following:

- Credit score: Most lenders require a good credit score before extending loans.

- Credit history: Lenders often review borrowers’ repayment behavior and financial responsibility.

- Insurance: Lenders may require you to provide evidence of appropriate insurance coverage for the construction project.

- Guarantee: Lenders may require personal guarantees depending on the loan type.

- Documentation: Provide all relevant documentation, including plans, proof of ownership, and property appraisal.

Contact prospective lenders to get the specific information and eligibility requirements.

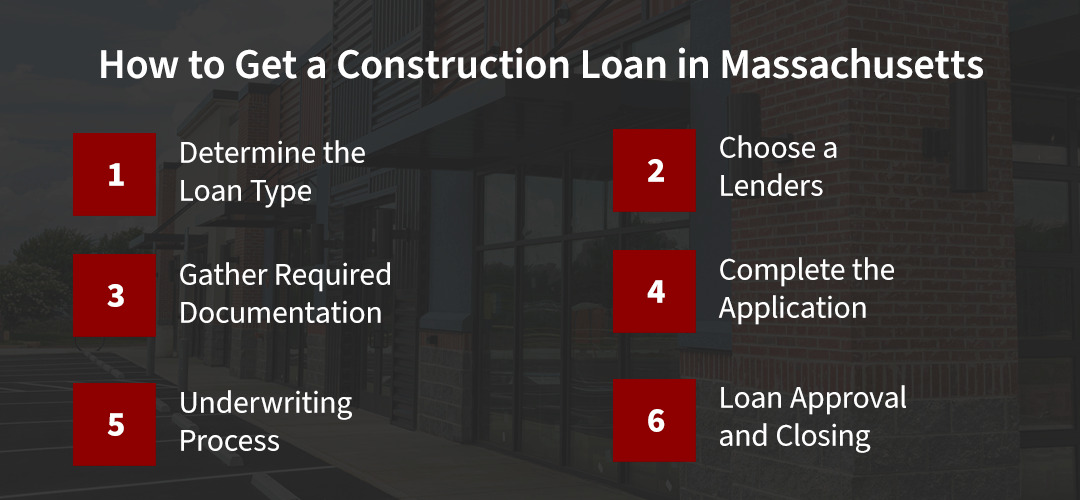

How to Get a Construction Loan in Massachusetts

Getting a CRE loan in Massachusetts involves several steps. Here is a step-by-step guide:

1. Determine the Loan Type

Research the loan type to determine repayment terms, including the duration and interest rates. Different loan types may also have slightly different application processes than the following steps.

2. Choose a Lenders

Research various lenders, including banks, credit unions, and private lenders. Consider factors like interest rates, fees, and customer service, where applicable. Also, verify information like how much you can borrow.

3. Gather Required Documentation

Prepare the necessary documentation for your application. This may include:

- Personal and business financial information: These include tax returns and financial statements.

- Project plans and specifications: Provide detailed construction plans, specifications, and a breakdown of the estimated construction costs.

- Builder or contractor information: Lenders may request credentials of the contractor or builder, including license and insurance. You may also be required to provide a signed construction contract.

- Land and property information: Gather proof of ownership or purchase agreements for the land where construction will occur. You may also need a current appraisal of the property.

- Permits and approvals: Collect any necessary permits required by local authorities. Add zoning approvals, if applicable.

4. Complete the Application

Fill out the lender’s application form and submit it with the gathered documentation. Some lenders may charge an application fee, so be prepared for this expense.

5. Underwriting Process

The lender reviews your application, including credit history, financial documents, and project feasibility. They may also conduct a site visit or inspection to assess the property and project.

6. Loan Approval and Closing

If the lender approves the loan, you’ll get a commitment letter detailing the loan terms. Review the documents carefully. Then, finalize the agreement by signing documents at a closing meeting. The lender will disburse funds according to the agreed-upon schedule.

Negotiating Construction and Real Estate Loan Agreements

Construction and real estate loan agreements can be complex, but take your time to review the terms and conditions. Consider the interest rates, repayment schedules, and any fees. Also, determine the penalties for late payments or changes in interest rates. Each construction project is unique, so tailor the agreement to suit your needs. For example, you can negotiate repayments or draw schedules according to milestones. Here are some negotiation strategies:

- Research current market conditions, the lender’s priorities, and standard loan terms.

- Set clear objectives, including the desired loan amount, interest rates, and contingencies.

- Build rapport during the negotiation and maintain open lines of communication.

- Document discussions, agreements, and changes made during the negotiation process

- Use legal counsel to review the loan agreement and protect your interests.

Why Trust Us?

Calabrese Law Associates is a leading law firm based in Massachusetts. Our knowledgeable attorneys have years of experience navigating the legal aspects of CRE loans and have worked on complex real estate and construction projects. This background has given us an insight into what most businesses in the industry need.

We are committed to providing personalized and effective legal solutions to clients. We assess matters case-by-case, allowing us to develop practical strategies. Our reputation is built on trust, transparency, and open communication. Again, our attorneys take time to listen to concerns, ensuring that clients are informed and supported at every step of the process.

When you pick Calabrese Law Associates, you choose a partner who genuinely cares about your success and is dedicated to achieving your best possible results.

Contact the Real Estate and Construction Loan Attorneys at Calabrese Law Associates

Real estate and construction loan laws protect borrowers and regulate transactions with lenders. It is essential to learn these laws and understand loan agreements to protect your interests. An attorney can advise, review agreements, and provide legal representation where necessary.

Want to know more about CRE loan regulations or need legal assistance? Contact Calabrese Law Associates today for professional guidance. Our experienced attorneys can help you navigate complex legal requirements, ensure compliance, and protect your interests. Don’t leave your future to chance — schedule a consultation with us now!

This publication and its contents are not to be construed as legal advice nor a recommendation to you as to how to proceed. Please consult with a local licensed attorney directly before taking any action that could have legal consequences. This publication and its content do not create an attorney-client relationship and are being provided for general informational purposes only.

Attorney Advertising. Prior results do not guarantee a similar outcome.